Words matter. These are the best Economists Quotes from famous people such as Stephen J. Dubner, David Autor, John Sulston, Richard Thaler, Annalee Newitz, and they’re great for sharing with your friends.

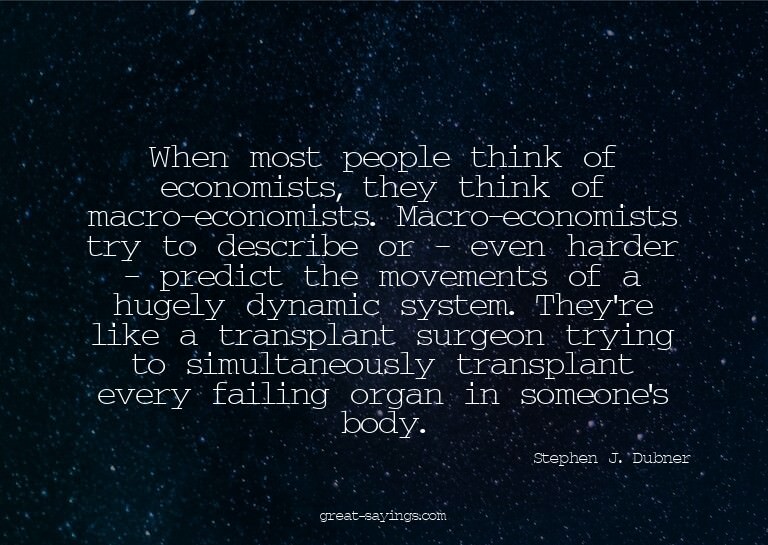

When most people think of economists, they think of macro-economists. Macro-economists try to describe or – even harder – predict the movements of a hugely dynamic system. They’re like a transplant surgeon trying to simultaneously transplant every failing organ in someone’s body.

I think we labor economists like to think of ourselves as being closer to the people.

I’m pleased that some economists and sociologists are beginning to talk about, for example, alternative measures of human well-being – alternative, that is, to GDP, on which the world runs.

The sad truth is that many behavioral economists know very little about psychology.

In the 1970s, as historians became enchanted with microhistories, economists were expanding the reach of their discipline. Nations, states and cities began to plan for the future by consulting with economists whose prognostications were shaped by investment cycles rather than historical ones.

As economists bandy about terms like ‘recapitalization,’ ‘credit lines,’ and ‘liquidity,’ families are facing brutal cuts to their social services and welfare payments, losing their homes, wondering how their kids will make their way in the world.

There must have been something in the air of Gary that led one into economics: the first Nobel Prize winner, Paul Samuelson, was also from Gary, as were several other distinguished economists.

Instead of a universal basic income, we could have a basic income guarantee. Or, as economists prefer to call it, a negative income tax.

In the 1960s, and stretching back to the 1930s, it was felt by many economists that easy money is a reliable way to increase employment.

Indeed, willingness to challenge professional economists and other experts is a foundation stone of democracy. If all we have to do is to listen to the experts, what is the point of having democracy?

Some economists believe that the Greeks’ work ethic and thrift can pull them through. But the classical virtues can do nothing to offset the dearth of innovation that plagues the economy.

Contrary to what professional economists will typically tell you, economics is not a science. All economic theories have underlying political and ethical assumptions, which make it impossible to prove them right or wrong in the way we can with theories in physics or chemistry.

Perhaps concentrated wealth will inspire a nation of innovative problem-solvers. But if the view of many economists is right – that it sometimes discourages innovation – then we should worry.

I have always been considered to be the most German among Italian economists, which I always received as a compliment, but was rarely meant to be one.

I’ve felt for some time that economics needs to be taught differently by economists who actually have had experience making a payroll or investing on Wall Street. When economics is taught by pure academics, watch out.

The traditional story of economists has been to say education explains what the returns are to school. I say, ‘Okay, that’s fine, but what explains the education? How much is just a matter of my giving you a poor kid versus a rich kid?’

Economists are coming to acknowledge that measures of national wealth and poverty in terms strictly of average income tell you little that is significant of the health or viability of a society.

I think Obama and the economists around him have a very sophisticated understanding of both globalization and the technology revolution and the impact they’re having on the world economy and they way they’re creating these winner-take-all spirals.

When the Smoot-Hawley bill landed on President Herbert Hoover’s desk, more than 1,000 economists urged him to veto it. Tragically, the president ignored their pleas.

There’s a rising tide of concern among activists, economists, and artists about Africa. Theres a temptation to think of it as a monolith as opposed to all these different countries with different problems.

Economists actually disagree about whether there are significant economic returns from attending an elite college versus a less-selective one.

Economists must always be prepared for surprises: they find many in trying to find order in the universe of their study.

Some economists seem to think that only a credentialed economist has the right to be utterly wrong about an issue of economics. Their contempt for amateurs – columnists with broad audiences, for example – would sear the lungs if inhaled.

Many scientists and economists also say putting a price on carbon through carbon taxes and/or cap-and-trade is necessary.

Raising the minimum wage, as President Obama proposed in his State of the Union address, tends to be more popular with the general public than with economists.

Some economists estimate that for every family that goes bankrupt, there are about 15 more who are in the same amount of financial trouble and would profit from bankruptcy but just haven’t filed.

With more than 67 percent of the Nation’s freight moving on highways, economists believe that our ability to compete internationally is tied to the quality of our infrastructure.

I have arrived at the conviction that the neglect by economists to discuss seriously what is really the crucial problem of our time is due to a certain timidity about soiling their hands by going from purely scientific questions into value questions.

In terms of the Green New Deal, I support the urgency and the end goal of the Green New Deal. I would look to work with our climatologists, economists to propose my own plan and how we would meet those goals.

Most economists use ‘fixed’ and ‘pegged’ as interchangeable or nearly interchangeable terms for exchange rates.

The biggest tab the public picks up for fossil fuels has to do with what economists call ‘external costs,’ like the health effects of air and water pollution.

People today don’t become economists to make the world a better place.

Fortunately, economists open to new ways of thinking are finding novel ways to use supposedly irrelevant factors to make the world a better place.

I don’t think we should run government based on economists’ predictions.

Happiness quantification sounds a bit wishy-washy, sure, and through a series of carefully administered surveys across the globe, economists and psychologists have certainly confronted a fair number of sticky issues around how to measure, and even define, happiness.

Although most Americans apparently loathe inflation, Yale economists have argued that a little inflation may be necessary to grease the wheels of the labor market and enable efficiency-enhancing changes in relative pay to occur without requiring nominal wage cuts by workers.

Economists who have studied the relationship between education and economic growth confirm what common sense suggests: The number of college degrees is not nearly as important as how well students develop cognitive skills, such as critical thinking and problem-solving ability.

The role of the media in economic management is not often recognised even by professional economists. Politicians, however, ignore this at their own peril.

In the late 1960s, the New Classical economists saw the same weaknesses in the microfoundations of macroeconomics that have motivated me. They hated its lack of rigor. And they sacked it.

The greatest economic power might in fact remain in the hands of the Federal Reserve. Economists credit the Fed’s policy of keeping interest rates at historic lows with helping to pump up the economy and bring unemployment down.

I may be only a fish and chip shop lady, but some of these economists need to get their heads out of the textbooks and get a job in the real world. I would not even let one of them handle my grocery shopping.

A lot of people are surprised economists are assisting with kidney exchanges. Exchanges are what economists are good at.

Talking with economists, climate scientists, and psychologists convinced me that depersonalizing climate change, such that the only answers are systemic, is a mistake of its own. It misses how social change is built on a foundation of individual practice.

We are all amateur attention economists, hoarding and bartering our moments – or watching them slip away down the cracks of a thousand YouTube clips.

But the age of chivalry is gone. That of sophisters, economists, and calculators has succeeded; and the glory of Europe is extinguished forever.

Thirty years ago, many economists argued that inflation was a kind of minor inconvenience and that the cost of reducing inflation was too high a price to pay. No one would make those arguments today.

Psychologists and economists love to talk about the notion of two selves: present self and future self. It’s a nice way to explain the tendency to have one preference about the future, but a very different preference when the future becomes the present.

Parents, teachers, professors, economists, pundits, entrepreneurs, tinkerers and misfits all have to do a better job of unapologetically singing the praises of capitalism and free markets which unequivocally demonstrate the ability to pull people out of poverty and improve and lengthen their lives.

My folks are economists and have taught economics and social science so I grew up with those kind of conversations around the dinner table.